March 2023 Market Update

As I consider the Market of the Moment this month, I’m reminded of a quote I’ve always kept near and dear to my heart (and absolutely did not see for the first time when I just searched “Interesting Quotes About Markets” on Google…”

““An investment in knowledge pays the best interest.” ”

Now, to be fair, I did once visit the house in London where Ben Franklin lived FOR FREE for ten years so one can assume he was definitely a savvy real estate navigator. But regardless of his original audience, I think this maxim perfectly sums up the moment in which we all find ourselves in this tricky local housing market. An ounce of current market data is worth a pound of insight into whether or not you should buy or sell!

So without battering you with too many more Franlinesque puns, allow me to give you a sense of how we here at Pollock Properties Group feel that knowledge is the key to clarity.

The headline topics in our market continue to be two fold:

A generational demographic shift is bringing newly formed Millennial families out of their expensive 2BR apartment rentals in search of more space in which to live and work.

The rise in interest rates from under 3% to over 7% in a matter of months, coupled with positive financial factors in the lives of sellers, has led to an environment where current owners are not incentivized to sell.

First up, the buyers. Life and economics are all about alternatives. For the Millennial/first time buyers in our region, they are mostly having to decide between continuing to spend money on ever increasing rents in Brooklyn or “overpay” for a home in the suburbs.

s a useful aside in this conversation, I highlight the flawed logic of overpaying for real estate by my passive aggressive use of scare quotes! There is no price tag in a dynamic market for a limited resource; there is only the value of that resource constantly being set by other transactions. Even in an environment of increasing monthly costs, the thing that most matters to the buyer is being able to service a fixed debt against their variable income. And in a moment of inflation pushing wages higher and higher, it’s no surprise that the demand pool for houses in our area has not yet dried up amid such high prices.

With all this in mind, we are seeing buyers get creative with financing while offering a bit less to sellers. This does NOT mean that prices are going down but that the growth of those prices has certainly slowed a bit. We are still seeing a great amount of multiple bids in this area and the (yet to be made public) accepted offer prices our team is aware of shows an 8-13% jump between list price and sale price. This is down from the last couple years where that jump was much higher, but this Spring Market is still one of price inflation.

On the other side of the ledger, think about a typical seller who bought in Maplewood in the spring of 2011. They settled into a 3BR/1.5BA for a “Great Recession Sale” price of around $400K. But now their family of two has grown to a family of four and one full bathroom just doesn't cut it! They would love to move to a bigger home but they refinanced in 2020 at 3% and are feeling those golden handcuffs tightly around their wrists as they pay that low, low payment each month.

One thing that is eternally true in real estate though is that when children become teenagers, no one wants to share a bathroom with them anymore. Or is that just me with my four kids? Either way, homeowners primarily move because of life events and will worry about the finances second. Now this was easy to say when rates were close to the basement and it now feels like they are in the stratosphere. However, things are not as dire as they seem for our crowded family of four.

One silver lining in the current market is that the list price to sale price ratio for SOMA homes that list between $700K-$1M has been 3% higher than homes that list above $1M. This larger cut and the general price growth in this group, gives move-up buyers the ability to put more money down on their next home. This instant-equity is helping sellers borrow much less on their new, larger homes.

Sellers are also taking advantage of mortgage programs to pay down their rate or use variable arms to their advantage. Our mortgage partner Matt Keane can give prospective sellers great insights into what programs might help them the most.

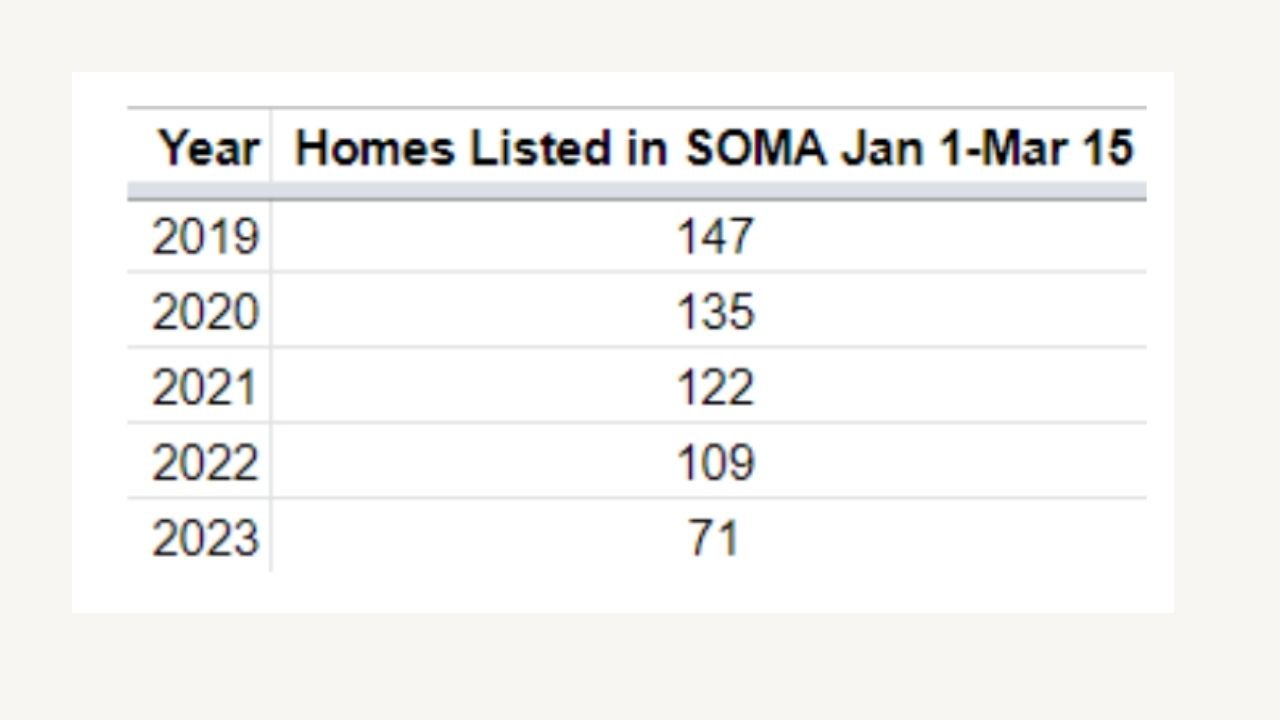

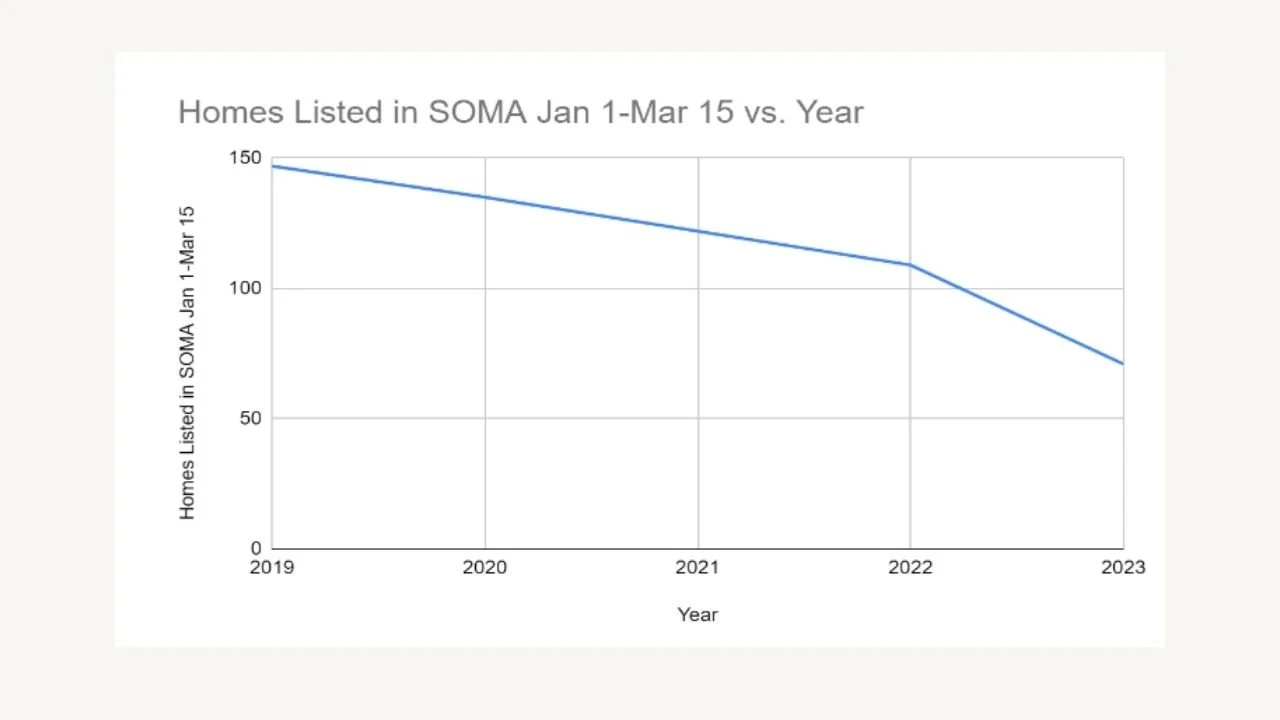

The final piece of data to share with you is just HOW drastic the decline in inventory has been. Below are two charts that show the homes listed from January 1st to March 15th for the past 5 years.

The obvious thing to glean from this information is that if you are planning on selling your home right now, it will sell and sell FAST. The supply is just too low for it to do otherwise. You can go from Poor Richard to Ben Franklin in one weekend! Ok, I’ll stop.

And if you are a buyer in Northern New Jersey today, our advice is that you get with a great mortgage broker like Matt Keane and find out what monthly payment works within your long term budget. Prices are not drastically changing anytime soon because it might take ten years for inventory to get back to 2019 levels. But purchasing a house now still presents more pros than cons over that same decade.

Give us a call today and we’ll show you how we can help!

KEVIN KERN

Realtor/Sales Associate

Pollock Properties Group of Keller Williams Realty Premier Properties

mobile: 917-405-6998 email: kevinkern@kw.com